Last updated: June 2026

Increasing the capital of a Colombian company may be necessary when the business needs additional funding, plans to admit a new investor, wants to strengthen its financial position or must document an investment for a corporate, banking or immigration procedure.

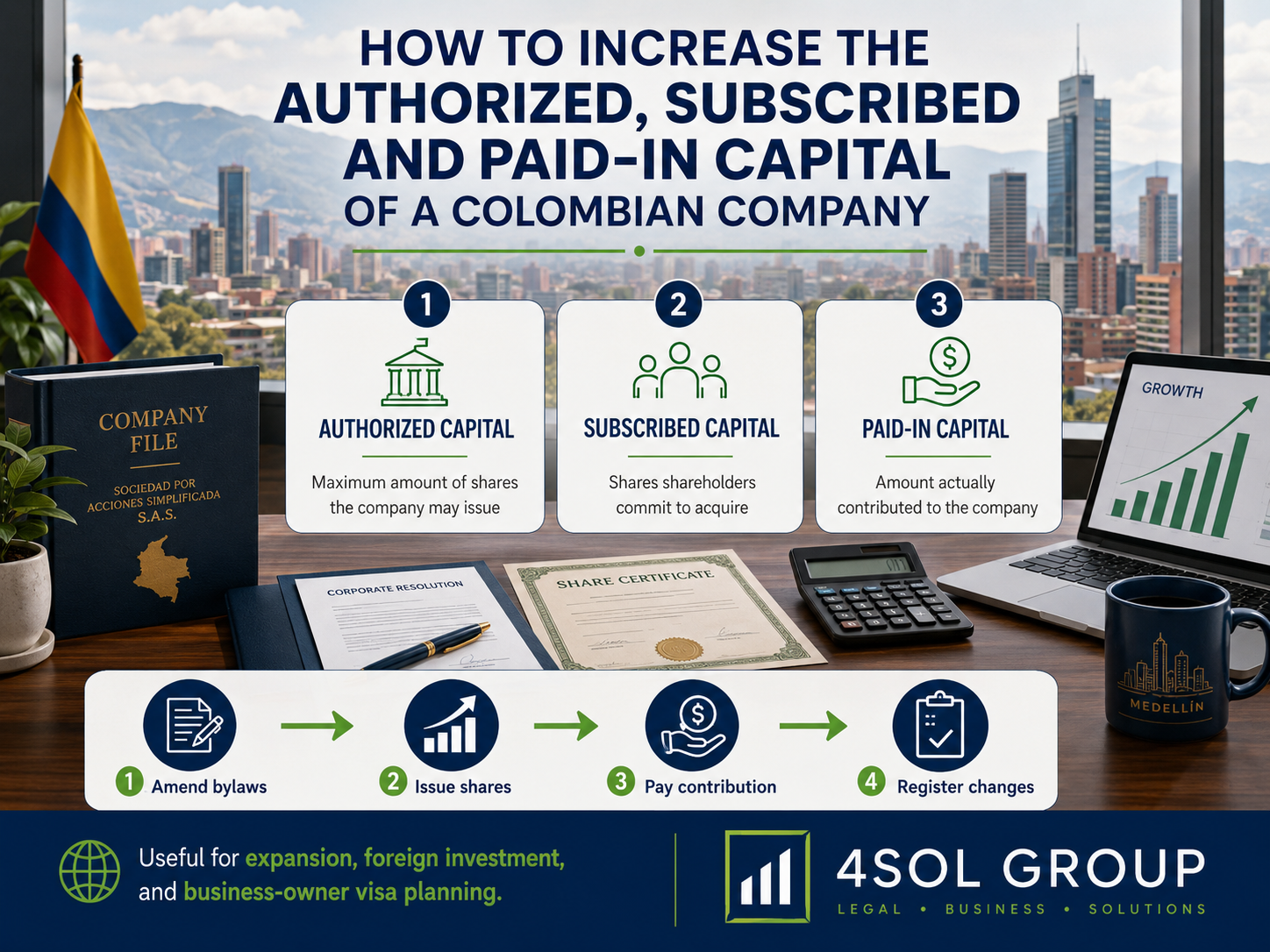

However, Colombian companies limited by shares do not have only one capital figure.

Their corporate structure generally distinguishes between:

- Authorized capital

- Subscribed capital

- Paid-in capital

These amounts are related, but they do not represent the same thing. Increasing one figure does not necessarily increase the other two.

For example, increasing the authorized capital only expands the company’s legal capacity to issue shares. It does not prove that an investor acquired shares or transferred money to the company.

This guide explains how to increase the authorized, subscribed and paid-in capital of a Colombian company, with particular emphasis on the Colombian Simplified Stock Corporation, known as a Sociedad por Acciones Simplificada or SAS.

Which Colombian Companies Use Authorized, Subscribed and Paid-in Capital?

The authorized, subscribed and paid-in capital structure generally applies to Colombian companies whose capital is divided into shares, including:

- Simplified Stock Corporations — SAS

- Stock Corporations — Sociedad Anónima or SA

- Partnerships Limited by Shares — Sociedad en Comandita por Acciones

This terminology does not operate in exactly the same manner for every type of Colombian legal entity.

For example, a limited liability company, known as a Sociedad de Responsabilidad Limitada, has a capital structure divided into ownership quotas rather than shares.

Because the SAS is the most common corporate vehicle for entrepreneurs and foreign investors in Colombia, this article focuses primarily on that structure.

Understanding the Three Types of Capital

Before approving a capital increase, the shareholders must understand what each capital figure represents.

Authorized capital

Authorized capital is the maximum nominal amount of shares that the company is legally permitted to issue under its bylaws.

It functions as a statutory ceiling.

The authorized capital is calculated using:

Number of authorized shares × nominal value per share

If the company has:

- 100,000 authorized shares

- A nominal value of COP 1,000 per share

its authorized capital is:

COP 100,000,000

The company is not required to issue all authorized shares immediately.

The difference between the authorized shares and the subscribed shares generally constitutes the shares available in reserve for future issuance.

Increasing the authorized capital normally requires a formal amendment to the company’s bylaws.

Subscribed capital

Subscribed capital is the portion of the authorized capital that shareholders have agreed to acquire and pay.

It is calculated using:

Number of subscribed shares × nominal value per share

If shareholders have subscribed 50,000 shares with a nominal value of COP 1,000 each, the subscribed capital is:

COP 50,000,000

The shareholder’s obligation arises from the subscription of the shares, even when the entire amount has not yet been paid.

Subscribed capital can never exceed authorized capital.

Paid-in capital

Paid-in capital is the portion of the subscribed capital that has actually been contributed to the company.

Payment may occur through mechanisms such as:

- Cash contributions

- Bank transfers

- Contributions in kind

- Capitalization of qualifying receivables

- Capitalization of profits or dividends

- Other legally valid contribution mechanisms

If the shareholders subscribed COP 50,000,000 and paid the full amount, the company would report:

- Subscribed capital: COP 50,000,000

- Paid-in capital: COP 50,000,000

If they paid only COP 30,000,000, the figures would be:

- Subscribed capital: COP 50,000,000

- Paid-in capital: COP 30,000,000

- Outstanding subscribed capital: COP 20,000,000

For an SAS, the payment deadline established for subscribed shares cannot exceed two years.

Comparison of the Three Capital Figures

| Capital type | What it represents | Does it mean money was received? | Main procedure |

|---|---|---|---|

| Authorized capital | Maximum amount of shares the company can issue | No | Statutory amendment |

| Subscribed capital | Shares shareholders committed to acquire | Not necessarily | Share issuance and subscription |

| Paid-in capital | Amount effectively contributed | Yes, or another valid contribution | Payment and corporate certification |

When Does a Company Need to Increase Its Authorized Capital?

The company must generally increase its authorized capital when it does not have enough unissued shares available to complete the proposed transaction.

For example, assume a company has:

- Authorized capital: COP 100,000,000

- Subscribed capital: COP 100,000,000

- Paid-in capital: COP 100,000,000

Because the authorized and subscribed capital are equal, the company has no shares in reserve.

If it wants to issue an additional COP 80,000,000 in shares, it must first increase its authorized capital.

By contrast, assume the company has:

- Authorized capital: COP 200,000,000

- Subscribed capital: COP 100,000,000

- Paid-in capital: COP 100,000,000

In this case, it has COP 100,000,000 in shares available for future subscription, assuming the nominal value and share structure remain unchanged.

The company may be able to increase its subscribed capital without first amending the authorized capital.

Does Increasing Authorized Capital Increase the Company’s Assets?

No.

Increasing authorized capital does not by itself:

- Transfer money to the company

- Create a completed investment

- Increase cash in the company’s bank account

- Prove that shares were acquired

- Increase paid-in capital

- Register a foreign investment

- Satisfy an investor visa requirement

It only increases the maximum amount of share capital that may legally be issued.

A complete capitalization may require several separate corporate and financial steps.

Step 1: Review the Company’s Current Records

Before preparing the capital increase, the company should review:

- Current Chamber of Commerce certificate

- Bylaws

- Authorized, subscribed and paid-in capital

- Number of authorized shares

- Number of subscribed shares

- Number of paid shares

- Nominal value per share

- Classes and series of shares

- Shareholders’ ledger

- Existing shareholder percentages

- Subscription and payment deadlines

- Shareholders’ agreements

- Restrictions on issuing or transferring shares

- Rights of first refusal or preference

- Previous capital increase documents

The figures shown in the bylaws, Chamber of Commerce records, accounting records and shareholders’ ledger should be consistent.

Any discrepancy should be corrected before completing a new capitalization.

Step 2: Determine the Final Capital Structure

The company should establish the intended final figures before preparing the corporate documents.

For example:

Current structure

- Authorized capital: COP 100,000,000

- Authorized shares: 100,000

- Subscribed capital: COP 50,000,000

- Subscribed shares: 50,000

- Paid-in capital: COP 50,000,000

- Paid shares: 50,000

- Nominal value: COP 1,000 per share

Intended final structure

- Authorized capital: COP 200,000,000

- Authorized shares: 200,000

- Subscribed capital: COP 180,000,000

- Subscribed shares: 180,000

- Paid-in capital: COP 180,000,000

- Paid shares: 180,000

- Nominal value: COP 1,000 per share

In this example, the company must address both:

- The increase of the authorized capital from COP 100 million to COP 200 million.

- The subscription and payment of an additional 130,000 shares, equivalent to COP 130 million.

The documentation must identify who acquires those shares and how the contribution is paid.

Step 3: Approve the Increase of Authorized Capital

Because authorized capital is stated in the bylaws, changing it generally constitutes a statutory amendment.

The shareholders’ assembly or sole shareholder must approve the modification.

The decision should clearly state:

- Current authorized capital

- New authorized capital

- Current number of authorized shares

- New number of authorized shares

- Nominal value per share

- Classes of shares, when applicable

- Exact amendment to the relevant bylaw

- Voting result

- Effective date of the amendment

For an SAS, the applicable approval majority should first be verified in the bylaws.

In the absence of a special statutory rule, the legal default generally allows statutory amendments to be approved by shareholders representing at least one-half plus one of the shares present at the meeting.

A company with a sole shareholder must record the decision in a duly prepared written minute.

Step 4: Prepare the Shareholders’ Meeting Minutes

The minutes should comply with Colombian corporate law and the company’s bylaws.

They should ordinarily include:

- Company name

- NIT

- Type of meeting

- Date and place of the meeting

- Method and date of notice

- List of attendees

- Number of shares represented

- Verification of quorum

- Agenda

- Proposal for the capital increase

- Explanation of the transaction

- Final capital figures

- Number and nominal value of shares

- Approval of the statutory amendment

- Approval of any related share issuance

- Voting results

- Authorization to complete the filing

- Signatures of the chair and secretary

- Approval of the minutes

The minutes must be internally consistent.

A common filing problem occurs when the total capital does not equal the number of shares multiplied by their nominal value.

Step 5: Register the Authorized Capital Increase

The statutory amendment must be filed with the Chamber of Commerce corresponding to the company’s principal domicile.

Depending on the transaction, the filing may include:

- Certified copy of the minutes

- Private statutory amendment document

- Public deed, when legally required

- Filing forms

- Evidence of payment of registration fees

- Evidence of payment of the applicable registration tax

- Powers of attorney, when filed through a representative

Registration fees and taxes depend on the jurisdiction, the type of document and the value of the transaction.

The company should obtain an updated Chamber of Commerce certificate after registration and verify that the authorized capital appears correctly.

Step 6: Approve the Issuance and Placement of Shares

Increasing authorized capital does not automatically increase subscribed capital.

To increase subscribed capital, the company must issue and place shares.

The appropriate corporate body must approve the issuance under:

- The bylaws

- Applicable shareholders’ agreements

- Existing share classes

- Rights of preference

- Restrictions on share ownership

- Applicable corporate law

Depending on the structure, the company may need a formal share issuance and placement regulation, known in Spanish as a reglamento de emisión y colocación de acciones.

The issuance documents may address:

- Number of shares offered

- Class of shares

- Nominal value

- Subscription price

- Payment method

- Payment deadline

- Persons entitled to subscribe

- Exercise of preemptive rights

- Waiver of preemptive rights

- Offer period

- Acceptance procedure

- Consequences of non-payment

Share Subscription Price vs. Nominal Value

The nominal value of a share is the value assigned to it in the company’s capital structure.

The subscription price is the amount the investor pays to acquire the share.

These amounts do not always have to be identical.

For example, a share may have:

- Nominal value: COP 1,000

- Subscription price: COP 1,500

The difference of COP 500 may be recorded as a share premium, known as a prima en colocación de acciones.

Only the nominal value increases subscribed capital.

The premium is generally recorded separately within the company’s equity.

Companies should therefore avoid increasing the nominal value merely to reflect the commercial or market value of the business without analyzing the corporate, accounting and tax consequences.

Step 7: Respect Existing Shareholder Rights

Issuing new shares may dilute the ownership percentages of existing shareholders.

Before approving the issuance, the company must review:

- Statutory preemptive rights

- Rights of first refusal

- Special share classes

- Voting rights

- Anti-dilution provisions

- Minimum or maximum ownership percentages

- Shareholders’ agreements

- Restrictions applicable to new investors

Example:

A company has two shareholders:

- Shareholder A: 70%

- Shareholder B: 30%

If new shares are issued only to Shareholder A, Shareholder B’s percentage may decrease.

The issuance must therefore comply with the rights established in the bylaws and any valid shareholders’ agreement.

A capital increase should not be used improperly to dilute, exclude or prejudice a minority shareholder.

Step 8: Execute the Share Subscription

The investor must formally accept and subscribe for the shares.

Depending on the transaction, the documentation may include:

- Share subscription agreement

- Acceptance of the share offer

- Share issuance regulation

- Shareholders’ decision

- Proof of payment

- Investment agreement

- Contribution agreement

- Capitalization agreement

- Waiver of preemptive rights

- Representations regarding the source of funds

The subscription documents should identify:

- Subscriber

- Number of shares acquired

- Class of shares

- Nominal value

- Subscription price

- Total contribution

- Amount paid immediately

- Outstanding balance

- Payment deadline

- Payment method

Step 9: Pay the Subscribed Shares

Paid-in capital increases only when the company actually receives the contribution or when another legally valid capitalization is completed.

Common payment methods include:

Cash contribution

The shareholder transfers or deposits money into the company.

The company should retain:

- Bank records

- Transfer confirmations

- Payment receipts

- Accounting entries

- Source-of-funds documents

Capitalization of a shareholder loan

A valid debt owed by the company to a shareholder may, under an appropriate corporate procedure, be converted into equity.

The company should verify:

- Existence of the debt

- Accounting recognition

- Loan agreement

- Applicable foreign exchange registration

- Accrued interest

- Corporate approval

- Tax consequences

A loan should not be converted into capital only through an accounting entry without the required corporate authorization.

Capitalization of profits or dividends

Retained earnings, approved dividends or other qualifying equity accounts may be capitalized through the appropriate shareholder decision.

The supporting financial statements and accounting treatment must be consistent with the transaction.

Contribution in kind

The investor may contribute an asset rather than money, such as:

- Equipment

- Vehicles

- Intellectual property rights

- Shares in another company

- Real estate

- Other legally transferable assets

The asset must be properly identified, valued and transferred to the company.

When the contribution includes real estate or another asset whose transfer requires a public deed or special registration, the capitalization must comply with those additional formalities.

Step 10: Register the Increase in Subscribed and Paid-in Capital

Changes to subscribed and paid-in capital must be registered before the Chamber of Commerce of the company’s principal domicile.

Depending on the cause of the increase, the supporting document may be:

- Certificate issued by the statutory auditor

- Certificate issued by the company’s public accountant

- Shareholders’ meeting minutes

- Public deed

- Other applicable corporate document

The certificate should generally identify:

- Company name and NIT

- Nominal value per share

- Total number of subscribed shares

- Total subscribed capital

- Total number of paid shares

- Total paid-in capital

- Cause of the increase

- Relevant subscription or payment date

- Deadline of the share offering, when applicable

As a general registration rule, the increase in subscribed capital should be reported within the period calculated from the expiration of the share subscription offer, and the paid-in amount should be reported within the applicable period following the payment deadline or completion of the offering.

The company should coordinate the filing promptly with its lawyer and accountant rather than waiting until the information is needed for a bank, investor or visa application.

Step 11: Update the Shareholders’ Ledger

The company must update its shareholders’ ledger to reflect:

- Name of each shareholder

- Identification information

- Number of shares

- Class of shares

- Acquisition date

- Subscription details

- Payment status

- Ownership percentage

- Transfers or encumbrances, when applicable

The shareholders’ ledger is fundamental evidence of share ownership.

Registration of the company’s capital before the Chamber of Commerce does not replace the need to keep the internal shareholders’ ledger updated.

The company should also issue or update share certificates when appropriate.

Step 12: Update the Accounting Records

The company’s accounting should distinguish between:

- Authorized capital

- Subscribed capital

- Subscribed capital pending payment

- Paid-in capital

- Share premium

- Shareholder loans

- Contributions in kind

- Capitalized profits

- Other equity accounts

Corporate documents, accounting records and Chamber of Commerce information must tell the same financial and legal story.

An accountant should not record a contribution as paid-in capital before the underlying corporate and financial transaction has occurred.

Capital Increase by a Foreign Shareholder

When a shareholder is a non-resident for Colombian foreign exchange purposes, the corporate capital increase may also constitute foreign direct investment.

The corporate procedure and the foreign exchange registration are separate but interconnected.

The company may need to coordinate:

- Shareholder approval.

- Share issuance and subscription.

- International transfer of funds.

- Correct foreign exchange declaration.

- Foreign investment registration.

- Accounting recognition.

- Chamber of Commerce filing.

- Update of the shareholders’ ledger.

- Obtaining the foreign investment extract.

If the money enters Colombia through an authorized foreign exchange intermediary and is correctly declared as foreign investment, registration may occur automatically based on the exchange transaction.

If the investment originates from a qualifying transaction that does not require currency channeling, a direct registration may be required through the Banco de la República’s Foreign Exchange Information System.

A corporate capital increase registered with the Chamber of Commerce does not, by itself, register the foreign investment.

Capital Increases and Colombian Investor Visas

A capital increase may be relevant for certain Colombian investor or business-owner visa applications.

However, increasing the company’s authorized capital alone is insufficient.

The visa authority may examine:

- Subscribed capital

- Paid-in capital

- Identity of the foreign shareholder

- Ownership percentage

- Shareholders’ ledger

- Company certificate

- Accounting certificate

- Bank transfer

- Foreign exchange declaration

- Foreign investment extract

- Source of funds

- Continuity of the investment

- Company’s actual economic activity

The applicable minimum investment threshold should be verified at the time of filing because it may be calculated using Colombia’s current legal minimum monthly wage.

A capital increase should reflect a real transaction. Corporate documents created without an actual contribution may expose the company and its administrators to legal, accounting, immigration and tax risks.

Complete Capital Increase Example

Assume a Colombian SAS currently reports:

- Authorized capital: COP 100,000,000

- Subscribed capital: COP 50,000,000

- Paid-in capital: COP 50,000,000

- Nominal value: COP 1,000 per share

The sole shareholder wants the final structure to be:

- Authorized capital: COP 200,000,000

- Subscribed capital: COP 180,000,000

- Paid-in capital: COP 180,000,000

The procedure may involve:

1. Statutory amendment

Increase authorized capital from COP 100 million to COP 200 million.

The number of authorized shares increases from 100,000 to 200,000 while maintaining the COP 1,000 nominal value.

2. Share issuance

Issue and subscribe an additional 130,000 shares.

3. Payment

The shareholder contributes COP 130 million to the company.

4. Corporate records

Update the shareholders’ ledger and supporting subscription documents.

5. Chamber of Commerce registration

Register the final subscribed and paid-in capital.

6. Accounting

Record the contribution accurately.

7. Foreign investment registration

When the shareholder is a qualifying non-resident, verify that the additional investment is correctly registered with the Banco de la República.

At the end, 20,000 shares remain available in reserve:

- Authorized shares: 200,000

- Subscribed shares: 180,000

- Shares in reserve: 20,000

Documents Commonly Required

Depending on the transaction, the company may need:

- Current Chamber of Commerce certificate

- Current bylaws

- Shareholders’ meeting or sole shareholder minutes

- Statutory amendment

- Share issuance and placement regulation

- Subscription agreement

- Waivers of preemptive rights

- Accountant or statutory auditor certificate

- Proof of payment

- Bank statements

- SWIFT confirmation

- Foreign exchange declaration

- Foreign investment extract

- Contribution-in-kind valuation

- Public deed

- Updated shareholders’ ledger

- Updated share certificates

- Accounting certificate

- Power of attorney

Common Capital Increase Mistakes

1. Increasing only the authorized capital

The company increases its statutory ceiling but does not issue, subscribe or pay new shares.

The updated certificate shows greater authorized capital, but no new equity investment has been completed.

2. Allowing subscribed capital to exceed authorized capital

A company cannot validly subscribe more shares than it is authorized to issue.

The authorized capital must first be increased when there are insufficient shares in reserve.

3. Confusing payment with subscription

Transferring money to a company does not automatically issue shares.

The corporate subscription procedure must also be completed.

4. Issuing shares without reviewing dilution

The company issues shares to one investor without calculating the effect on existing ownership percentages.

5. Ignoring preemptive rights

The company admits a new investor without respecting rights granted to existing shareholders.

6. Using inconsistent capital figures

The minutes show one amount, the accountant’s certificate shows another and the mathematical calculation produces a third amount.

7. Changing the nominal value unintentionally

The company increases the capital but fails to clarify whether it is increasing the number of shares, the nominal value or both.

8. Failing to update the shareholders’ ledger

The Chamber of Commerce certificate is updated, but the internal ownership records remain unchanged.

9. Registering corporate capital but not foreign investment

A foreign shareholder contributes funds and receives shares, but the foreign exchange transaction is reported incorrectly.

10. Treating a shareholder loan as capital

Money previously recorded as debt is later described as paid-in capital without completing a lawful capitalization.

11. Using a capital increase only to support a visa application

The company prepares documents showing a larger investment without matching bank, accounting and foreign exchange evidence.

12. Missing registration deadlines

The company completes the subscription and payment but delays the Chamber of Commerce filing.

Frequently Asked Questions

Must authorized, subscribed and paid-in capital always be equal?

No.

A company may have authorized capital greater than subscribed capital and subscribed capital greater than paid-in capital.

However:

- Subscribed capital cannot exceed authorized capital.

- Paid-in capital cannot exceed subscribed capital.

Does increasing authorized capital mean the company received money?

No. Authorized capital is only the maximum amount the company is permitted to issue.

Can subscribed and paid-in capital be increased at the same time?

Yes. When shares are subscribed and paid immediately, both figures may increase as part of the same transaction.

Does every capital increase require a statutory amendment?

Not necessarily.

Increasing authorized capital normally requires a statutory amendment.

Increasing subscribed capital within the existing authorized capital may not require an amendment to the authorized-capital clause, but the issuance, subscription and registration procedures must still be completed.

How long does a shareholder have to pay subscribed shares in an SAS?

The payment terms may be established in the bylaws, issuance documents or subscription agreement, but the payment period cannot exceed two years.

Can a foreigner increase the capital of a Colombian company?

Yes. Foreign individuals and companies may invest in a Colombian company, subject to corporate, foreign exchange, tax, compliance and beneficial ownership requirements.

Can a loan be converted into company capital?

Potentially, yes. The debt, corporate approval, accounting treatment and foreign exchange implications must be reviewed before capitalization.

Can real estate be contributed to the company?

Yes, subject to valuation, shareholder approval, public deed, property registration, taxes and other applicable requirements.

Does the Chamber of Commerce verify that the money was actually paid?

The registry examines the documents submitted for registration. The company, its administrators, accountant, statutory auditor and shareholders remain responsible for the truth and accuracy of the information.

Does a capital increase guarantee approval of an investor visa?

No. The visa authority evaluates the entire transaction and the applicant’s compliance with immigration requirements.

How 4Sol Group Can Help

At 4Sol Group, we assist Colombian companies and foreign investors with the complete legal and financial structure of corporate capital increases.

Our services may include:

- Reviewing the company’s bylaws and current capital structure

- Calculating the required authorized, subscribed and paid-in capital

- Preparing shareholders’ meeting or sole shareholder minutes

- Drafting statutory amendments

- Preparing share issuance and subscription documents

- Reviewing preemptive rights and shareholder dilution

- Coordinating accountant and statutory auditor certifications

- Filing the capital increase before the Chamber of Commerce

- Updating shareholder ownership records

- Coordinating international transfers

- Registering foreign investment with the Banco de la República

- Obtaining foreign investment extracts

- Aligning the corporate transaction with an investor visa application

- Reviewing the tax and accounting documentation with the company’s accountant

A properly completed capital increase requires more than filing a single meeting minute.

The company’s bylaws, share issuance, payment records, accounting, shareholders’ ledger, Chamber of Commerce registration and foreign investment records should all be consistent.

Contact 4Sol Group before transferring investment funds or approving a capital increase in a Colombian company.

Legal notice: This article provides general information and does not constitute individual legal, tax, accounting, immigration or foreign exchange advice. The requirements applicable to a capital increase depend on the company type, bylaws, shareholders, contribution method, jurisdiction and purpose of the transaction.

Contact us or request an appointment for professional advisory services.

Contact us or request an appointment for professional advisory services.